Guest Essay - The Rise (and Fall) of Pandemic Learning Pods

Hello!

The following essay is the first of two guests posts on Learning Pods. There are two reasons I am publishing these guest posts:

I am curious about Learning Pods, but don’t know where I stand on the topic. The authors of the posts know more about Learning Pods than I do and I believe we all benefit hearing from them directly.

I would like EdTech Thoughts to grow into a space that asks questions about the education industry. As you will see, the authors have fairly different points of view on where Learning Pods are headed. This is a good thing! I am excited for them to lay out their thoughts so that you can consider (or re-consider) your own

This is an experiment. I would like to publish more content from both myself and others in 2023, but want to do a trial run now to collect feedback. After these two posts, it will be roundups-only until my 2023 predictions in December.

With that, let’s meet our first author, Jack McDermott!

Author Spotlight

The most rewarding part of growing this newsletter has been meeting (and debating ideas with) folks plugged in all over the education ecosystem. Meeting our guest author, Jack McDermott, is a perfect example of this stroke of fortune. He is thoughtful, data-driven, and consistently pushes me to sharpen my perspective.

Jack McDermott is a product and growth leader with experience at edtech companies in a variety of verticals. He holds an MBA and M.Ed from the University of Virginia Darden School of Business and can be reached via his website or LinkedIn

The Rise (and Fall) of Pandemic Learning Pods

Of the many edtech trends stemming from the pandemic, perhaps the most interesting was the rise of learning pods. With school doors closed and Zoom fatigue setting in, many parents (and some districts) sought a better, in-person option to combat the limitations of remote learning.

Enter learning pods.

What are learning pods?

Small groups of ~4-8 children who meet for in-person learning (typically at a private residence)

Staffed by one educator (typically a former teacher / paraprofessional)

Non-standard curriculum (typically emphasizing self-directed learning)

Supported by a tech-enabled platform (typically aiding in scheduling, curriculum, and payments)

In late 2020, learning pods grew from the grassroots, often organized via Facebook Groups and parents’ text message chains. Edtech investors soon took notice.

Schoolhouse raised $8M and Prenda got $20M for their pursuits of scaling learning pods and microschools. If you’ve been following for a while, you may remember AltSchool, which raised over $175M between 2013-2016 for a nationwide network of microschools with physical campuses. Learning pods gained sizable funding and press headlines as public schools remained closed to in-person learning in 2021-2022.

Disaggregating “full stack” education

While companies like Schoolhouse, Prenda, and AltSchool created unique services, all shared in an endeavor to disaggregate different layers of “full stack” education.

A sample of four common layers of educational services that comprise any school’s stack. (This could surely be expanded into dozens of additional or more detailed layers).

American schools provide many more services than the delivery of instruction alone; schooling is as much curriculum and instruction as it is a physical place, staffing of teachers and administrators, and technologies that serve a variety of academic and non-academic purposes.

The strategy of microschools can be generally summarized as disintermediating the supply of some (or all) of these services from public schools to parents as consumers. Each company decided where and how to “unbundle” this full stack of services into a unique, alternative offering that most appeals to parents.

AltSchool chose to aggregate the full stack by providing physical campuses with curriculum, staffing, and a homegrown tech platform, others chose to unbundle one or multiple layers. Bubbles, for example, provided professional staffing for at-home learning pods; while Schoolhouse brought curriculum, staffing, and tech together, but parents provided their homes as a physical footprint.

The great return to in-person school

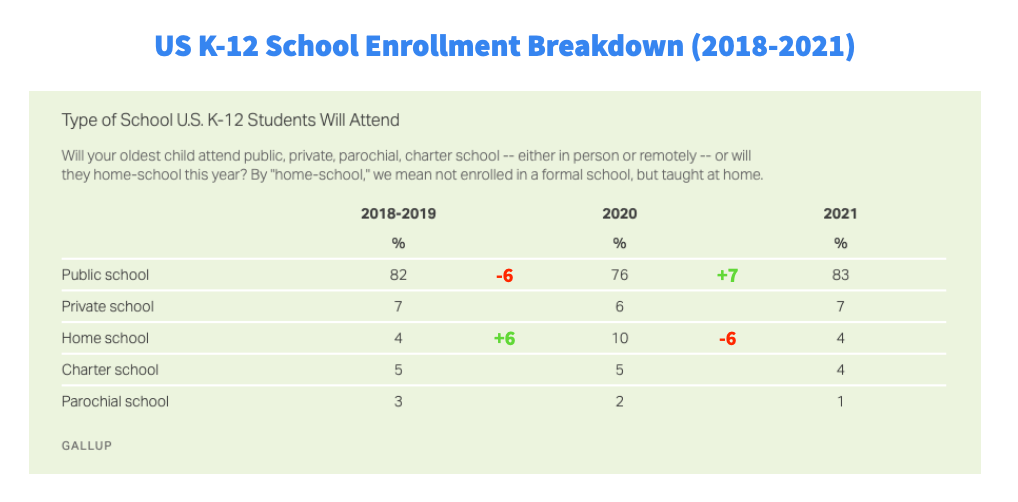

Approximately 3% of school-aged children in the US are homeschooled. This figure remained constant for a decade; then, at the peak of the pandemic, homeschooling represented upwards of ~10% of students per Gallup parent surveys.

Parents opted into homeschooling at ~2.5X their usual rates during COVID, likely heightening interest in learning pods. While the survey data are imperfect (i.e., only asking about oldest child, lack of detail into what form of homeschooling, etc.), the magnitude and directions of these swings is remarkable.

Inflows into homeschooling appear correlated to outflows from public schools during the peak of the pandemic according to Gallup surveys.

Homeschooling now appears to have returned to historical enrollment levels. The one-year boom in at-home learning now looks like a regression to the mean.

What’s driving this trend? It appears that parents of public school students opted into homeschooling, only to return to public schools a year later. “Home school” was selected by parents +6% points more frequently in 2020 and -6% points less in 2021. Directionally, these are the same and inverse enrollment deltas seen by—you guessed it—public schools.

So students are returning to public schools and our mix of K-12 education settings now looks more like its pre-pandemic norm than anything materially different.

Building a $100M/year business

The jump in homeschooling in 2020 and sizable investment into learning pods companies begs the question: can you build an enduring, sizable education business in this space?

To answer that question, let’s use a hypothetical “billion-dollar edtech test”—what would have to be true for an edtech startup to reach $100 million in revenue within 10 years? This simple heuristic helps explain how venture investors eyeing a 10X return might evaluate the merits of any particular startup.

An intentionally-messy diagram depicting how four learning pods / microschools companies chose to unbundle different layers of a school’s stack.

Let’s focus on a company unbundling the “tech” layer of the schooling stack—a SaaS platform that enables learning pods. To me, a bet on a learning pods platform of this kind likely requires a combination of tailwind trends:

1. A greater share of K-12 parents will opt their kids into homeschooling in future years

You could imagine learning pods winning student enrollment away from traditional public schools. This looks like creating an alternative system for elementary and secondary education.

2. Parents will spend significantly more on supplementary learning services

Learning pods could benefit from increased supplementary education spending by parents, even those with students enrolled in public schools. This looks more like additional out-of-school tutoring and learning services.

3. Reopening local public schools will take longer and be less desirable to parents

A third bet is the pandemic recovery—and subsequent re-opening of schools—would be more L-shaped than V-shaped. That is, it would take longer and be more difficult to bring students back into public schools in the near-term—a trend that does not appear to be playing out—creating more opportunities for learning pods to potentially win over parents and students.

Back-of-napkin math

So let’s model it out, back-of-napkin.

Assume you run a learning pods tech platform that charges ~$10,000 per year in tuition per student (paid by semester, with some likely churn), spends ~90% of tuition on teacher salaries, and has gained enough product-market fit to win ~1 in every 100 parents of homeschoolers to pay at this price point.

I start with these assumptions because they aren’t too far off from how learning pods operated within the last year. Here’s Schoolhouse CEO Brian Tobal on the company’s business model:

Tuition varies depending on pod size and location, but tuition for a pod of eight students in locations like New York and California would be around $7,386 per student per semester for five hours of school a day, five days a week, according to SchoolHouse’s website. Tobal said 90 percent of tuition goes toward teachers’ salaries.

Quick math shows that a learning pods SaaS platform would likely need to win ~80% of a significantly larger addressable target market to reach $100M in net revenue/year.

You can think of many drivers of business success for tech-enabled learning pods platforms. But for simplicity, let’s take a company’s marketshare against competitors (y-axis) and the percentage of K-12 students in a “homeschool” setting (x-axis) to help us answer the what must be true to reach venture-scale question.

What this intentionally-simplistic math tells us is there’s a path towards building a $100M/year net revenue business in learning pods. But it’s likely a narrow one:

We start with our base assumptions holding true ($10K price point, ~1% target market penetration)

We assume our business model is a subscription SaaS / tech platform (net revenue from subscriptions, less the cost of what teachers/staff are paid)

You own 80% of the learning pods platform market

Homeschooling grows exponentially to serve ~26% of the 49.4 million students in US public schools today

If all holds true, you have a shot at building a $100M/year learning pods platform business. And perhaps that’s a company capable of delivering venture-scale returns.

There are other emerging avenues for building a compelling business in this space. States like Arizona and New Hampshire are amending education funding regulations to provide tax-supported education savings accounts (“ESAs”) to families. New services like Odyssey then facilitate tuition payment between families and microschools like Prenda. ESAs may remove the biggest barrier to microschool growth—the cost of tuition—and represent yet another disaggregated layer of full stack education.

You might also believe that parents will increase spending on supplemental learning for their children. That is, paying for tutoring, personalized lessons and small group learning, and other out-of-school academic services for kids. And there’s some evidence that parents did indeed increase their spending on supplementary learning services by ~10% during the pandemic.

Most parents cite using microschools to supplement their child’s existing education. Still, as investor Michael Milken has found, American households only spend ~2% of their income on supplemental learning, compared to ~15% by Asian households. There’s a long way to go towards achieving massive scale.

Looking ahead

During the pandemic, education systems conducted the largest scale experiment ever in remote learning. To me, learning pods represented the most natural response of an edtech solution to the pandemic

It’s too early to tell how entrants like Prenda and Schoolhouse will fare. But substitute teacher-matching company Swing Education shuttered its “Bubbles” learning pods service earlier this year.

In thinking back to AltSchool, the company ultimately abandoned its quest to build a nationwide network of microschools. There are differences, of course, between AltSchool and the pandemic crop of learning pods companies: AltSchool took a full-stack approach with physical campuses and teaching staff responsible for the soup-to-nuts delivery of learning.

But the lesson may be the same. AltSchool was reconstituted as Altitude Learning in 2019, opting to serve students with one layer of the stack (tech) and within the confines of their existing school system instead of creating an alternative system of its own.

Google searches for “learning pods” and “microschools” look like a blip during the height of COVID-19 school closures.

With another school year underway, it appears likely that learning pods may go the way of other pandemic era necessities: keychain door openers, Zoom happy hours, dots spaced out by 6-feet on grocery aisle floors, etc. All beneficial, convenient, and widespread during the pandemic era, but enduring to a far lesser extent.

Perhaps more than anything, the final lesson may be that American public schools—and parents’ choices to stay with them—are far more resilient than we give them credit for.

Ed Tech Thoughts is a short ( ~ 5 mins), weekly overview of the top stories in EdTech, with a few (hopefully interesting) gut reactions attached. If you enjoyed this guest post, I hope you will subscribe and/or forward to your friends!

If you would be interested in contributing a guest post to EdTech Thoughts in the future, please reply to this email and let us know!

| A guest post by

|

Excellent series on Education Pods and Full Stack Education. We seem to have decided as a nation to operate our K-12 educational system as a "Governmental System" rather than the front-line education of our children. Within the educational system, we have ignored innovation and continuous improvement, leaving that to the free market.

I am working on a new book now regarding the state of our educational system and these essays helped validate I was on the right track with certain aspects. Your Substack is much appreciated. Thanks!

David, Author of "Public Speaking for Kids, Tweens, and Teens: Success for Life!" (a previous book)

Pretty confused by the chart -- seems like it's off by a factor of... 100?

By my reckoning,

* 4% of ~50 million students is 2 million homeschoolers

* 100 million in revenue at a price point of $10k means 10e8/10e4 = 10e4, so 10k students

* 10k / 2 million is .005, so half a percent of homeschoolers.

So, you'd need to be off past the top left of the table to hit the 100m/yr figure... unless I'm missing factors that you're including.

Is there a hidden variable that you're including that I'm missing here?